High-Risk Activity Insurance: What Activities Are Covered?

Finding the right travel insurance can be tricky, especially when you're planning an adventure that pushes the limits. Is your standard travel insurance enough, or do you need something more specialized for high-risk activities? This article breaks down the key differences between high-risk insurance and standard travel insurance, helping you make the best choice for your adrenaline-fueled trip. We'll cover what's typically excluded from standard policies, what high-risk insurance covers, and even recommend some specific plans.

Understanding Standard Travel Insurance

Standard travel insurance is designed for typical vacation scenarios. Think delayed flights, lost luggage, or a sudden illness that requires a doctor's visit. It usually covers:

- Trip cancellation and interruption

- Lost or delayed baggage

- Medical expenses for illness or injury

- Emergency medical evacuation (sometimes, but often with limitations)

However, and this is a big *however*, standard policies often have exclusions. These exclusions are where high-risk activities come into play.

Why Standard Travel Insurance Often Fails for High-Risk Activities

Here's the deal: standard travel insurance policies are often designed for low-impact activities. They assume you'll be relaxing on a beach, visiting museums, or enjoying leisurely hikes. They *don't* anticipate you BASE jumping off a cliff or ice climbing in the Himalayas.

Common exclusions that will bite you when participating in high-risk activities include:

- Extreme sports: Activities like skydiving, paragliding, rock climbing (especially without proper safety gear), mountaineering, and certain types of skiing (heli-skiing, backcountry skiing) are frequently excluded.

- Activities outside designated areas: If you venture off marked trails or participate in activities deemed unsafe by local authorities, you might be on your own.

- Lack of proper certification or supervision: If you're scuba diving without a certified instructor or skiing off-piste without a guide, your claim could be denied.

- Intoxication: Injuries sustained while under the influence of alcohol or drugs are almost always excluded.

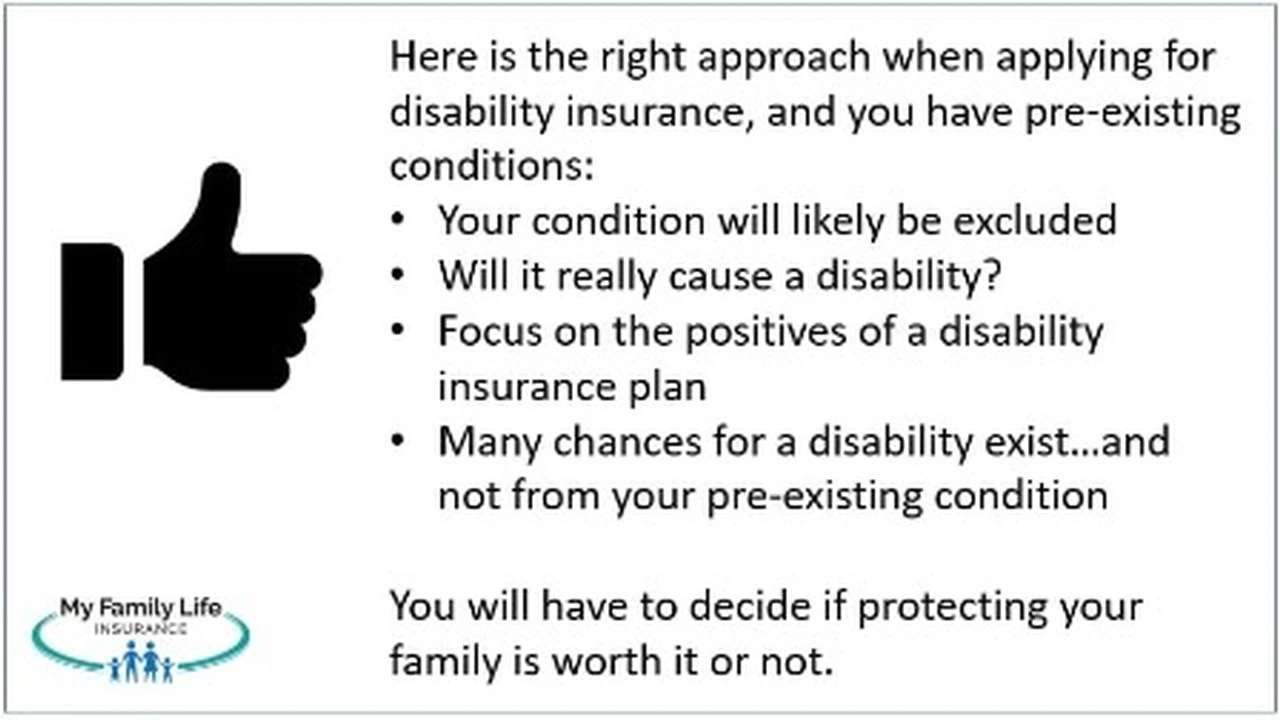

- Pre-existing conditions: While some standard policies offer limited coverage for pre-existing conditions, they often have restrictions that can leave you exposed during high-risk activities. The higher the risk, the more likely pre-existing conditions become a major problem with your coverage.

Basically, if your idea of a vacation involves pushing your physical limits or engaging in activities with a higher-than-average risk of injury, standard travel insurance likely won't cut it.

What is High-Risk Activity Insurance?

High-risk activity insurance, also sometimes called extreme sports insurance or adventure travel insurance, is specifically designed to cover activities that standard policies exclude. It provides broader coverage for the unique risks associated with these activities.

Here's what you can typically expect from a good high-risk activity insurance policy:

- Coverage for specific activities: The policy will clearly state which activities are covered. Make sure *your* activity is on the list!

- Higher medical expense limits: High-risk activities often lead to more serious injuries, so these policies offer higher limits for medical expenses, including hospitalization, surgery, and rehabilitation.

- Emergency medical evacuation coverage: This is crucial, as you might be in a remote location where getting to a hospital requires helicopter rescue or other specialized transportation. Look for policies with high evacuation limits.

- Search and rescue coverage: If you get lost or injured in a remote area, search and rescue operations can be incredibly expensive. High-risk policies often include coverage for these costs.

- Gear coverage: Specialized equipment for activities like climbing, diving, and skiing can be costly. Some high-risk policies offer coverage for lost, stolen, or damaged gear.

- Personal liability coverage: If you accidentally injure someone else or damage their property while participating in a covered activity, this coverage can protect you from financial loss.

Key Differences Summarized: High-Risk vs Standard Travel Insurance

Let's break down the key differences in a table for easy comparison:

| Feature | Standard Travel Insurance | High-Risk Activity Insurance |

|---|---|---|

| Activities Covered | Typical vacation activities (sightseeing, relaxing) | Specific high-risk activities (skydiving, climbing, etc.) |

| Medical Expense Limits | Lower limits | Higher limits |

| Emergency Evacuation | Often limited or excluded for high-risk situations | Comprehensive coverage, including helicopter rescue |

| Search and Rescue | Rarely covered | Often included |

| Gear Coverage | May cover lost luggage, but rarely specialized gear | May cover specialized gear (climbing equipment, diving gear) |

| Cost | Generally less expensive | Generally more expensive |

| Pre-existing Conditions | Limited coverage, often with strict requirements | May offer more comprehensive coverage, but often requires a medical assessment |

Specific High-Risk Insurance Plans and Scenarios

Okay, let's get into some specific examples. Keep in mind that policy details and pricing can change, so always get a quote and read the fine print before you buy.

World Nomads Explorer Plan for Adventurous Activities

Scenario: You're planning a multi-day backpacking trip through the Andes, including some moderate-level rock climbing. Why it's a good fit: World Nomads Explorer Plan is a popular choice for adventure travelers. It covers a wide range of activities, including rock climbing (up to a certain grade), trekking, and even some winter sports. It offers good medical expense limits and emergency evacuation coverage. Key Features: * Covers 200+ adventure activities * Emergency medical and dental coverage * Trip cancellation and interruption coverage * Gear protection * 24/7 emergency assistance Cost: Prices vary depending on your age, destination, trip duration, and coverage options. Expect to pay significantly more than a standard travel insurance plan. A rough estimate for a 2-week trip to South America for a 30-year-old could be around $200-$400. Get a quote on their website for accurate pricing. Pros: Wide range of covered activities, good reputation, flexible coverage options. Cons: Can be more expensive than some other options, may have limitations on pre-existing conditions.

IMG Signature Travel Insurance for Extreme Sports Enthusiasts

Scenario: You're a competitive paraglider traveling to Brazil for a championship event. Why it's a good fit: IMG Signature Travel Insurance offers comprehensive coverage for high-risk sports and activities, including paragliding, hang gliding, and other extreme sports. It provides high medical expense limits and emergency evacuation coverage, essential for these types of events. Key Features: * High medical expense and emergency evacuation limits * Coverage for extreme sports * Trip cancellation and interruption coverage * Accidental death and dismemberment coverage * 24/7 travel assistance Cost: Similar to World Nomads, expect to pay a premium for this level of coverage. A 2-week trip to Brazil could cost anywhere from $300-$500 or more, depending on your coverage options and age. Pros: Excellent coverage for extreme sports, high limits, reliable service. Cons: More expensive than some other options, may require a medical assessment for certain activities.

Divers Alert Network (DAN) for Scuba Diving and Freediving Adventures

Scenario: You're planning a liveaboard scuba diving trip in the Caribbean. Why it's a good fit: DAN is specifically designed for scuba divers and freedivers. It provides coverage for diving-related accidents, including decompression sickness, marine life injuries, and equipment loss. It also offers emergency medical evacuation coverage and access to a network of dive medical professionals. Key Features: * Coverage for diving-related accidents * Emergency medical evacuation coverage * Equipment loss coverage * Access to dive medical professionals * 24/7 emergency hotline Cost: DAN offers various membership levels and insurance plans. The cost will depend on the level of coverage you choose. An annual DAN membership with dive accident insurance can range from $100-$300 per year. Pros: Specialized coverage for divers, access to dive medical experts, reliable service. Cons: Only covers diving-related incidents, may not cover other travel-related issues.

Global Rescue for Remote and High-Altitude Expeditions

Scenario: You're attempting to summit Mount Kilimanjaro. Why it's a good fit: Global Rescue specializes in providing medical and security evacuation services for travelers in remote and challenging locations. They don't technically offer "insurance" in the traditional sense, but they provide membership-based evacuation and advisory services. Their services are invaluable for high-altitude mountaineering. Key Features: * Medical and security evacuation services * 24/7 medical and security advisory services * Field rescue services * Coordination with local authorities * Global network of medical and security professionals Cost: Global Rescue memberships can range from several hundred to several thousand dollars per year, depending on the level of coverage and the types of activities you'll be participating in. Pros: Expert evacuation services, global reach, reliable support. Cons: Expensive, doesn't cover medical expenses directly (works in conjunction with your primary health insurance or travel insurance).

Comparing High-Risk Insurance Products: A Quick Overview

Here's a simplified comparison table to help you quickly assess the different products mentioned above:

| Provider | Best For | Key Features | Approximate Cost (2-week trip) |

|---|---|---|---|

| World Nomads Explorer Plan | General adventure travel, backpacking, moderate-level activities | Wide activity coverage, good medical limits, gear protection | $200-$400 |

| IMG Signature Travel Insurance | Extreme sports, competitive events | High limits, comprehensive coverage for extreme activities | $300-$500+ |

| Divers Alert Network (DAN) | Scuba diving, freediving | Specialized coverage for diving accidents, access to dive medical experts | $100-$300 (annual membership) |

| Global Rescue | Remote expeditions, high-altitude mountaineering | Medical and security evacuation services, expert support | $Several hundred to several thousand (annual membership) |

Factors to Consider When Choosing High-Risk Insurance

Choosing the right high-risk insurance policy depends on several factors:

- Your activity: Make sure the policy specifically covers the activities you'll be participating in.

- Your destination: Some policies have geographic restrictions.

- Your medical history: Be honest about any pre-existing conditions.

- Your budget: Balance the cost of the policy with the level of coverage you need.

- The policy limits: Ensure the policy provides adequate coverage for medical expenses, emergency evacuation, and other potential costs.

- The fine print: Read the policy carefully to understand the exclusions and limitations.

Don't Skimp on Coverage: It's an Investment in Your Safety

While high-risk insurance can be more expensive than standard travel insurance, it's a worthwhile investment if you're planning adventurous activities. The cost of a medical evacuation or a serious injury in a remote location can easily run into the tens or even hundreds of thousands of dollars. Having the right insurance can protect you from financial ruin and ensure you get the medical care you need. So, before you pack your bags and head out on your next adventure, take the time to research and purchase the right high-risk insurance policy. Your peace of mind – and your wallet – will thank you.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)