Choosing the Right High-Risk Insurance Coverage Limits

Participating in high-risk activities? Selecting the right coverage limits is crucial for high-risk insurance. We explain how limits work and help you choose the best option for your needs and activity.

Understanding the Basics of High-Risk Activity Insurance Limits

Okay, so you're planning on doing something awesome… and probably a little crazy. Skydiving? Rock climbing? Maybe even BASE jumping? Whatever it is, you know you need insurance. But how much? That’s where coverage limits come in. Think of it like this: it's the maximum amount the insurance company will pay out if something goes wrong. Getting it right is crucial – too little, and you're on the hook for potentially massive bills. Too much, and you're throwing money away on premiums you don't need. Let's break it down.

Why High-Risk Activity Insurance Limits Matter: Real-World Scenarios

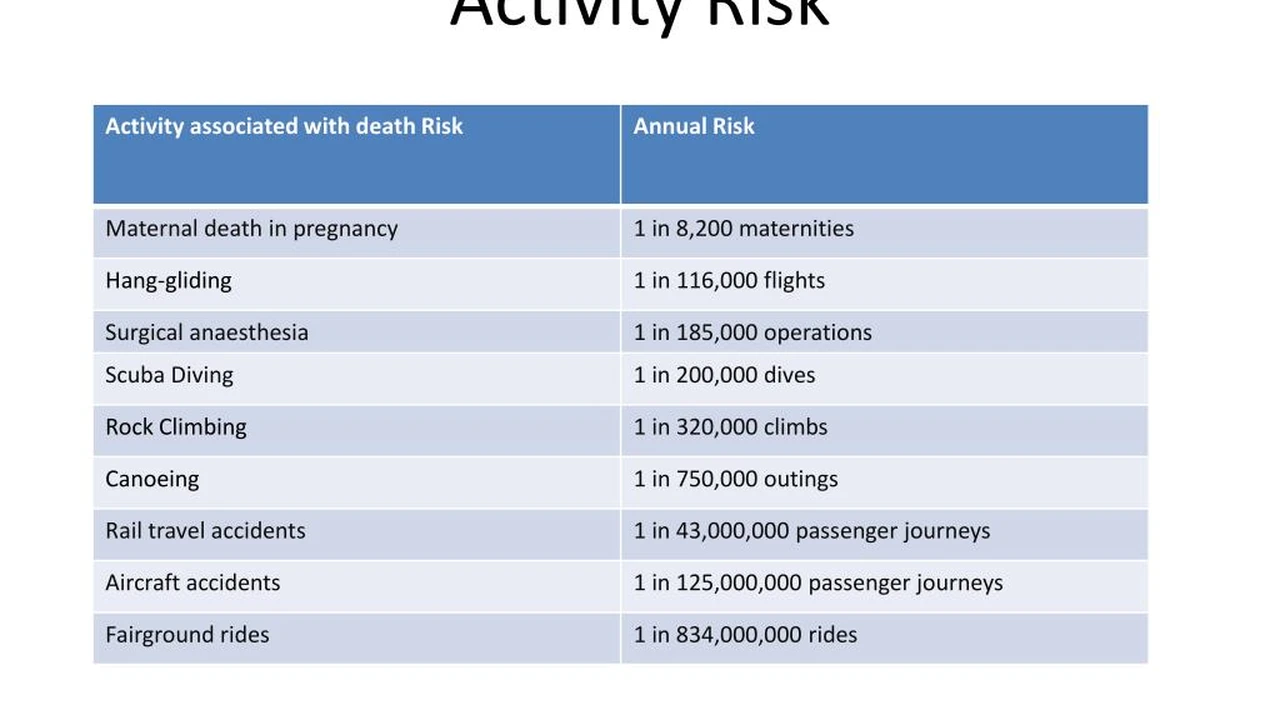

Let's face it, high-risk activities come with high-risk consequences. Imagine this: You're mountain biking in Moab, Utah, and you take a nasty spill, breaking your leg and requiring a helicopter evacuation. That helicopter ride alone can cost tens of thousands of dollars. If your insurance policy only covers $10,000 in medical evacuation, you're stuck paying the rest. Or picture this: you're scuba diving in the Great Barrier Reef, and you suffer a decompression sickness. Treatment in a hyperbaric chamber is essential, and that can easily run into thousands of dollars per session. Again, your coverage limit determines how much the insurance company pays and how much you pay out of pocket. These aren't just hypothetical scenarios; they happen all the time. That's why understanding and choosing the right coverage limits is so important.

Factors to Consider When Determining Your Ideal Coverage Amount: Risk, Destination, and More

So how do you figure out the right amount of coverage? It's not a one-size-fits-all answer. Here are the key factors to consider:

- The Specific Activity: Skydiving is generally riskier (and potentially more expensive if something goes wrong) than whitewater rafting. The higher the risk, the higher the coverage you'll likely need.

- Your Destination: Medical costs vary wildly around the world. Healthcare in the US is notoriously expensive. Remote locations often require costly medical evacuations. Research the average medical costs in your destination.

- Your Health Insurance: Will your existing health insurance cover you overseas? If so, how much? What are the deductibles and co-pays? Understanding your existing coverage is crucial to avoiding duplication and overpaying. Note: many US health insurance plans offer *very* limited or no coverage outside the US.

- Your Risk Tolerance: How comfortable are you with potentially paying out-of-pocket expenses? A higher deductible (the amount you pay before insurance kicks in) will lower your premiums, but it also means you'll be responsible for a larger initial expense.

- Policy Exclusions: Read the fine print! Some policies have exclusions for certain activities, pre-existing conditions, or specific locations. Make sure your policy actually covers what you plan to do.

Types of Coverage Limits to Evaluate: Medical, Evacuation, and Liability

High-risk activity insurance typically includes several different types of coverage, each with its own limit. Here's what to look for:

- Medical Coverage: This covers your medical expenses if you get injured or sick. Aim for a high limit, especially if you're traveling to a country with expensive healthcare. $100,000 is a good starting point, but consider higher amounts ($250,000 or more) for destinations like the US.

- Medical Evacuation Coverage: This covers the cost of transporting you to a hospital or medical facility. This is *crucial* for remote locations or activities where rescue can be difficult. Minimum $100,000 is recommended, and even higher for serious expeditions.

- Personal Liability Coverage: This protects you if you accidentally injure someone else or damage their property. While less common for individual adventure travel policies, it's worth considering, especially if you're participating in activities where you could potentially cause harm to others.

- Trip Cancellation/Interruption Coverage: This reimburses you for non-refundable trip costs if you have to cancel or cut your trip short due to a covered reason (illness, injury, etc.). Make sure the coverage amount is sufficient to cover all your pre-paid expenses.

- Gear/Equipment Coverage: If you're traveling with expensive gear (diving equipment, climbing gear, cameras), make sure your policy covers loss, theft, or damage. Note that some policies have limits on specific items.

Recommended High-Risk Activity Insurance Products and Coverage Levels

Alright, let's get into some specific recommendations. Keep in mind that prices and coverage options can change, so always check the provider's website for the most up-to-date information.

Product Recommendations:

- World Nomads Explorer Plan: This is a popular choice for adventure travelers. It offers comprehensive coverage, including medical, evacuation, trip cancellation, and gear protection. They cover a wide range of high-risk activities. They have different plans depending on your citizenship.

- Coverage Levels: You can typically choose medical coverage limits ranging from $100,000 to $500,000, and evacuation coverage up to $1,000,000. Gear coverage varies depending on the plan, but typically ranges from $500 to $2,500.

- Use Cases: Ideal for multi-sport adventures, extended trips, and travel to remote locations. Good for activities like trekking, climbing (below a certain altitude), scuba diving, and surfing.

- Price: Varies depending on your age, destination, trip length, and chosen coverage levels. Expect to pay anywhere from $100 to $500+ for a multi-week trip.

- IMG Signature Travel Medical Insurance: This plan focuses on robust medical coverage and is a solid choice if medical expenses are your primary concern.

- Coverage Levels: Medical coverage limits can range from $50,000 to $1,000,000. Evacuation coverage is typically included up to $500,000 or $1,000,000.

- Use Cases: Great for travelers concerned about high medical costs, particularly in the US or other countries with expensive healthcare. Less comprehensive on the trip cancellation/interruption side.

- Price: Generally competitive, especially if you prioritize medical coverage.

- Global Rescue: This isn't strictly insurance, but rather a membership-based service that provides medical, security, evacuation, and field rescue services. It's a good supplement to traditional insurance.

- Coverage Levels: Global Rescue focuses on providing the actual rescue and evacuation services, rather than paying out cash benefits. They coordinate and execute the rescue.

- Use Cases: Essential for serious expeditions, remote travel, and situations where traditional insurance might not be sufficient (e.g., political unrest, natural disasters).

- Price: Membership fees vary depending on the level of coverage and duration, but typically range from $300 to $1,000+ per year.

- Travel Guard AIG: Offers a variety of plans, some of which cover specific adventure activities. Check the policy details carefully.

- Coverage Levels: Varies significantly depending on the chosen plan. Read the policy wording carefully to understand the medical and evacuation limits.

- Use Cases: Good for travelers who want a well-known and established insurance provider.

- Price: Can be competitive, but requires careful comparison of different plans.

Comparing High-Risk Activity Insurance Products: World Nomads vs. IMG

Let's dive a little deeper and compare two popular options: World Nomads and IMG. Both are excellent choices, but they cater to slightly different needs.

- World Nomads: Known for its comprehensive coverage, especially for adventure activities. They have a user-friendly website and are generally well-regarded for customer service. They also allow you to purchase or extend your coverage while you're already traveling.

- IMG: Focuses primarily on medical coverage, often offering higher medical limits than World Nomads. They may be a better choice if you're primarily concerned about potential medical expenses. However, their coverage for trip cancellation/interruption and gear may be less extensive than World Nomads.

Here's a quick comparison table:

| Feature | World Nomads | IMG |

|---|---|---|

| Medical Coverage | Good, typically up to $500,000 | Excellent, can go up to $1,000,000+ |

| Evacuation Coverage | Typically up to $1,000,000 | Typically up to $1,000,000 |

| Trip Cancellation/Interruption | Comprehensive | Less comprehensive |

| Gear Coverage | Good | Varies, check policy details |

| Customer Service | Generally well-regarded | Generally well-regarded |

| Price | Competitive | Competitive |

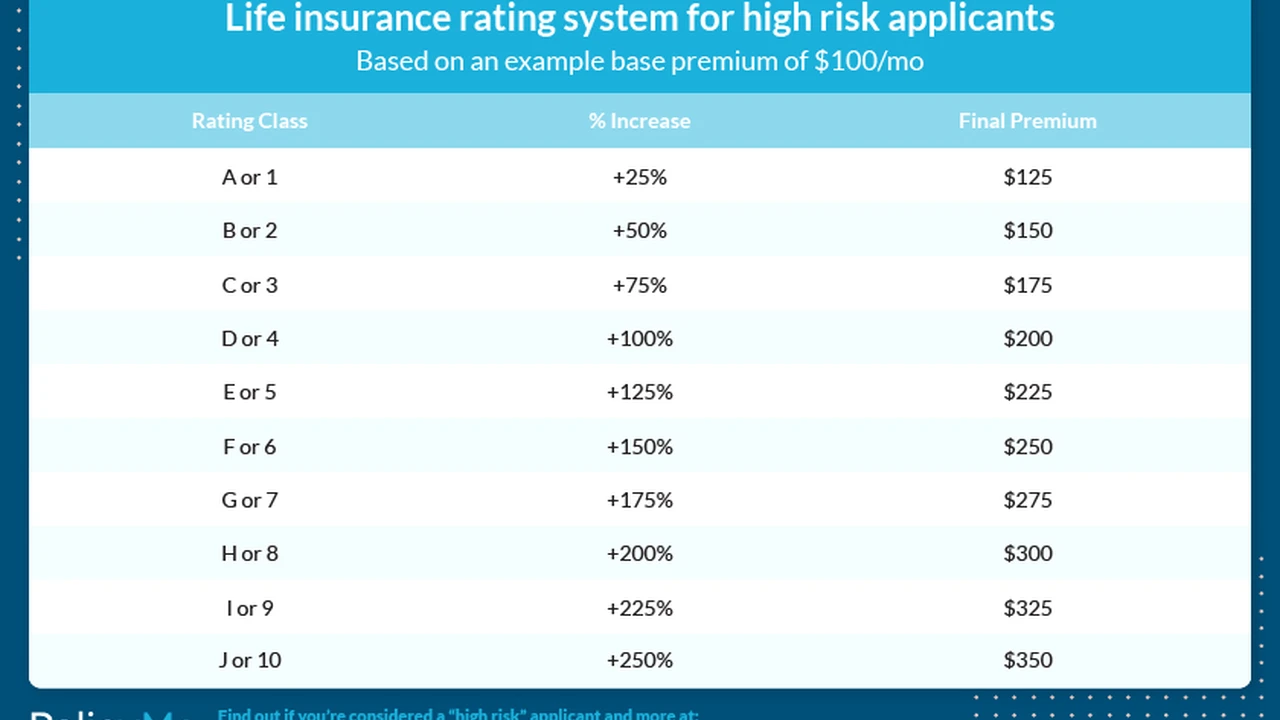

Understanding Deductibles and Policy Exclusions: The Fine Print Matters

Don't skip the fine print! Two crucial aspects of any insurance policy are the deductible and the exclusions.

- Deductibles: This is the amount you pay out-of-pocket before the insurance company starts paying. A higher deductible will lower your premium, but it also means you'll be responsible for a larger initial expense. Choose a deductible that you're comfortable paying.

- Exclusions: These are the specific situations or activities that the policy *doesn't* cover. Common exclusions include pre-existing conditions (unless specifically covered), participation in illegal activities, and injuries sustained while under the influence of alcohol or drugs. Make sure the policy covers the activities you plan to participate in.

Real-Life Examples: Choosing Coverage Limits for Specific Activities

Let's look at some specific examples to illustrate how to choose the right coverage limits:

- Rock Climbing in Yosemite: Given the remote location and potential for serious injuries, you'll want high medical and evacuation coverage. Aim for at least $250,000 in medical coverage and $500,000 in evacuation coverage. Consider Global Rescue membership as a supplement.

- Scuba Diving in Thailand: Medical costs in Thailand are relatively low, but decompression sickness can be expensive to treat. Aim for at least $100,000 in medical coverage, including coverage for hyperbaric chamber treatment.

- Backpacking in Europe: Medical costs vary across Europe, but are generally lower than in the US. Focus on trip cancellation/interruption coverage to protect your non-refundable travel expenses.

Tips for Saving Money on High-Risk Activity Insurance: Comparison Shopping and More

High-risk activity insurance can be expensive, but there are ways to save money:

- Comparison Shop: Get quotes from multiple providers and compare coverage levels and prices. Don't just focus on the lowest price; make sure the policy provides adequate coverage.

- Increase Your Deductible: A higher deductible will lower your premium.

- Choose the Right Coverage Levels: Don't over-insure yourself. If you already have health insurance that covers you overseas, you may not need as much medical coverage.

- Look for Discounts: Some providers offer discounts for students, groups, or members of certain organizations.

- Consider an Annual Plan: If you travel frequently, an annual travel insurance plan might be more cost-effective than purchasing individual policies for each trip.

The Importance of Reading Customer Reviews: Learn from Others' Experiences

Before you buy any insurance policy, read customer reviews. This can give you valuable insights into the provider's customer service, claims process, and overall reliability. Look for reviews on independent websites and forums, not just on the provider's own website. Pay attention to both positive and negative reviews, and try to get a sense of the overall consensus. Sites like Trustpilot and Squaremouth often host customer reviews for insurance providers.

Making the Final Decision: Balancing Cost and Coverage for Your Peace of Mind

Choosing the right high-risk activity insurance is a balancing act between cost and coverage. You want to get the best possible protection without breaking the bank. Carefully consider your specific needs, your destination, your risk tolerance, and your budget. Read the fine print, compare quotes, and don't be afraid to ask questions. Ultimately, the goal is to have peace of mind knowing that you're protected in case something goes wrong. So, do your research, make an informed decision, and then go out there and enjoy your adventure!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)